Categories

Buying Best Practices, Financing FAQPublished December 4, 2025

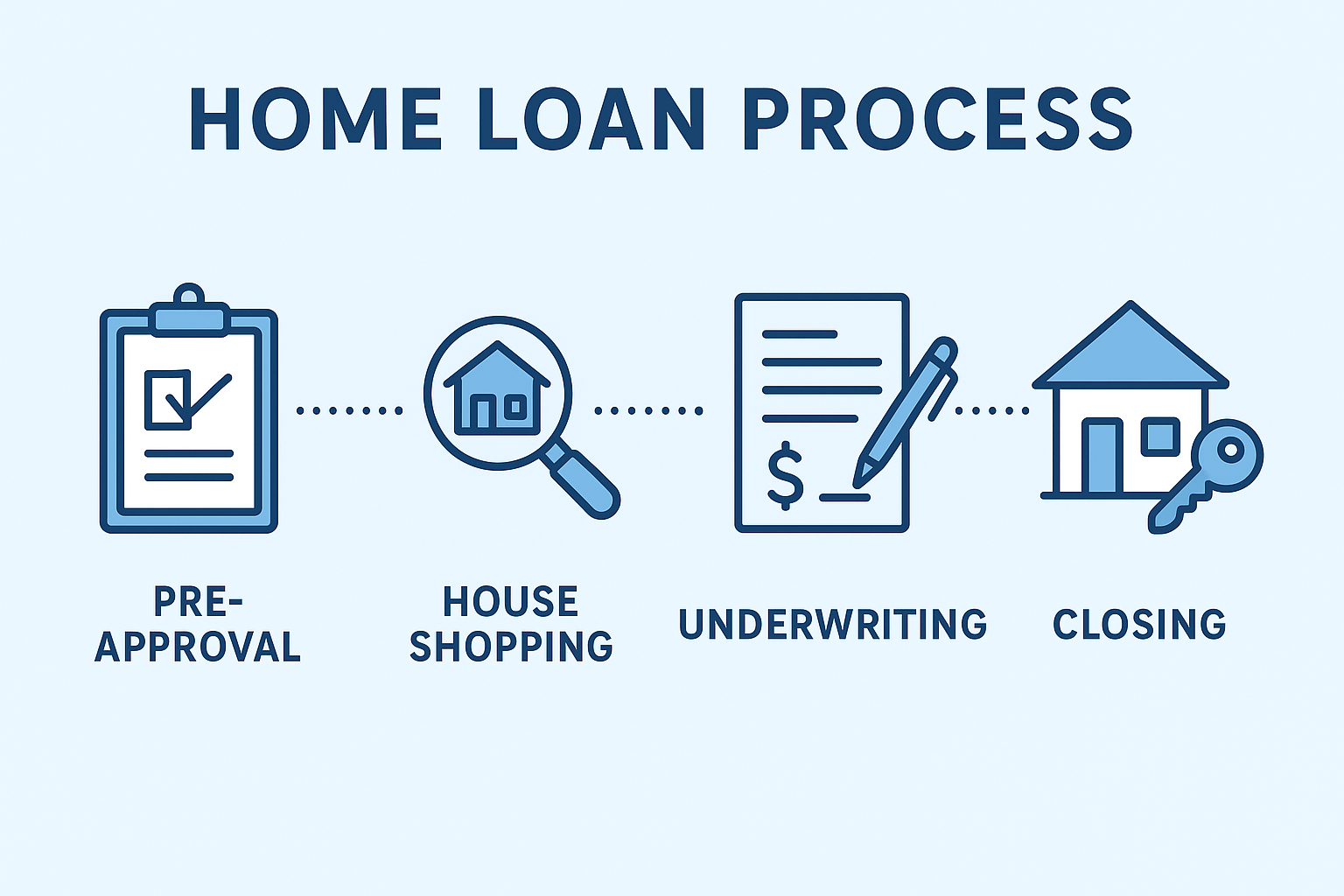

Understanding the Home Loan Process: A Brief Step-by-Step Guide

Understanding the Home Loan Process: A Brief Step-by-Step Guide

Buying a home is an exciting journey, and securing the right home loan is a crucial part of making your dream a reality. While the process may seem complex at first, breaking it down into clear steps can help you navigate it with confidence. Here’s an optimistic and straightforward guide to the home loan process to help you get started.

-

Assess Your Financial Health

You may be asking.

Where do I go for a loan? A bank or Mortgage professional.

What lender should I use? Which ever meets your needs and is a best fit for your financially.

What lender is local? There are several and we can discuss that.

How do I get a loan? You supply required paperwork to the loan officer depending on the loan you are trying to get.

What type of loan do I get? All depends on score, financing and where/what house you want to purchase.

These are all great questions.. However.

Before applying for a loan, take a close look at your financial situation. Check your credit score, review your income and expenses, and determine how much you can comfortably afford for monthly mortgage payments. A strong financial foundation will improve your chances of loan approval and better interest rates. ( which a great loan officer will do this with you, typically after a soft pull.) -

Get Pre-Approved

How long is my pre-approval good for? The lender can tell you that and update it as necessary.

What Is a pre approval? A letter stating you have been looked at and based on certain paperwork, you are loanable.

Where do I get one? Your lender gives you one during the process.

Getting pre-approved by a lender is a smart first step. This involves submitting financial documents such as pay stubs, tax returns, and bank statements. Pre-approval gives you a clear idea of your borrowing limit and shows sellers that you’re a serious buyer, giving you an edge in competitive markets. ( Not every situation or borrower is similar. Creating a custom personalized plan for you and your goals is best. ) -

Find the Right Home

What is the best website to search? Use your agents site or app to search.

Do I use Zillow to search? Using the agents app or site is best.

Does my agent have a site or app? - Yes we do.

With your pre-approval in hand, you can confidently shop for homes within your budget. Whether you’re looking for a cozy starter home or a spacious family residence, having a trusted real estate advisor by your side can make all the difference. They can help you find properties that meet your needs and negotiate the best deal. ( Yep, once we have it narrowed down on what type of financing and how much or if there are any grant restrictions on it. We can really narrow down the search with just that. ) -

Submit a Loan Application

Once you’ve chosen a home, it’s time to formally apply for your mortgage. Your lender will require detailed information about the property and your finances. This step initiates the underwriting process, where the lender evaluates your creditworthiness and the property’s value. -

Loan Processing and Underwriting

During this phase, the lender verifies all the information you provided, orders an appraisal to assess the home’s value, and reviews your financial documents. This thorough evaluation ensures that the loan meets all guidelines and that you’re a good candidate for financing. -

Loan Approval and Closing Disclosure

After underwriting, you’ll receive a loan commitment letter if approved. The lender will also provide a Closing Disclosure outlining the final loan terms, closing costs, and payment schedule. Review this document carefully and ask any questions you may have. -

Closing Day

On closing day, you’ll sign all necessary documents, pay closing costs, and finalize the mortgage. Once completed, you’ll receive the keys to your new home! This is the moment all your hard work and planning come together. -

Post-Closing

After closing, keep track of your mortgage payments and maintain communication with your lender. Staying organized and proactive will help you manage your loan successfully over time.

As always, you have freedom of choice. Choice to use whatever Lender, Home inspector, Insurance, Title company you want etc. We can provide options but ultimately it is your choice and we now have a form stating that just so you know.

As your dedicated real estate advisor, I’m here to guide you through every step of this process. Whether you need help finding the right home, connecting with trusted lenders, or understanding loan options, The Heilman Group is committed to your satisfaction. Feel free to reach out anytime at chris@heilman.group or call +1 740-277-3877. Together, we’ll make your homeownership dreams come true!

For more tips and updates, follow us on Facebook, Instagram, Twitter, and YouTube, or visit our website at https://forsalecolumbus.com. Let’s get started on your journey home today!

|

or another way